Article

Apr 8, 2026

How to Structure Equity When Co-Founders Contribute IP to a Startup

When co-founders contribute IP to a startup, equity structure gets complicated fast. Learn how to value contributions, document transfers, and avoid the disputes that kill companies.

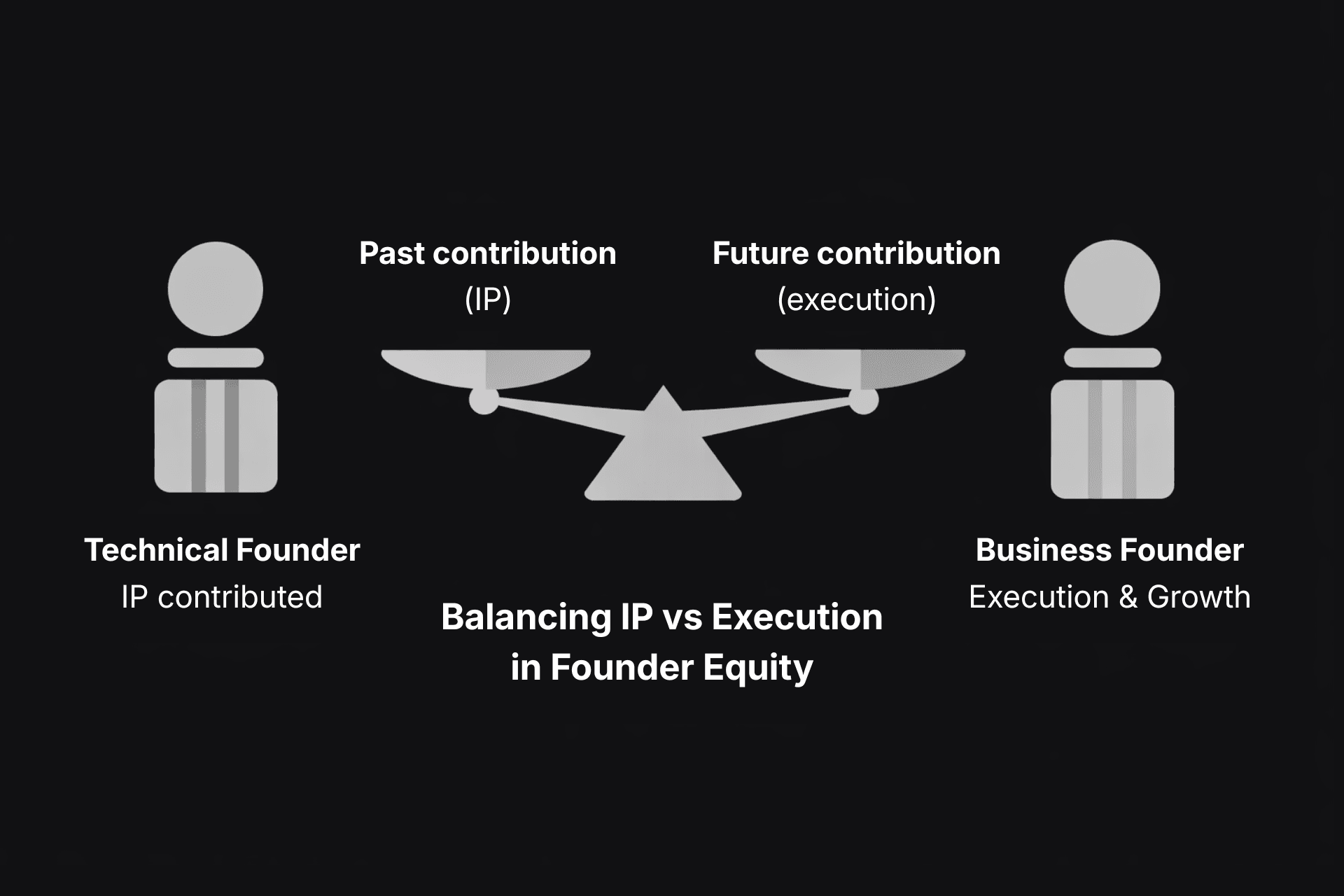

Equity splits between co-founders are difficult enough when everyone is contributing the same thing: time, effort, and commitment going forward. When one co-founder is also contributing intellectual property they created before the company existed, the conversation gets significantly more complicated.

The technical founder who spent two years building a machine learning model before recruiting a business co-founder. The researcher who developed a novel drug compound and is now starting a biotech with two operators. The engineer who wrote the core codebase and brought in a CEO and a designer to build a company around it. In each of these situations, someone is contributing something that already exists and already has value, and the question of how that contribution should be reflected in the equity split is one that founders get wrong more often than they get right.

Getting it wrong has real consequences. Equity disputes between co-founders are one of the leading causes of early-stage startup failure. IP ownership disputes that surface during fundraising kill deals. And founders who feel they were undercompensated for their IP contributions carry resentment that degrades working relationships long before it becomes a legal dispute.

This post explains how to think about the equity structure when IP is part of the founding contribution, how to document the transfer correctly, and how to build a structure that holds up to investor scrutiny and the test of time.

Why IP contributions complicate the equity conversation

In a standard co-founder equity split, the relevant inputs are forward-looking: who is going to do what, how much time is each person committing, what roles are they taking on, and what is each person's relative contribution to the company's success going forward. The equity split is essentially a bet on future contribution.

When one founder is contributing existing IP, the calculation changes. That IP represents past work, existing value, and often the core reason the company exists at all. Ignoring it in the equity split undervalues the contributing founder's position. Overweighting it ignores the reality that the IP is only valuable if the team can build a business around it.

The tension between these two perspectives is where most co-founder equity disputes originate. The technical founder feels their IP contribution entitles them to majority ownership regardless of what the other founders contribute going forward. The business co-founders feel that execution is where most of the value will be created and that the equity split should reflect future contribution. Both perspectives have merit, and the right structure needs to account for both.

Valuing IP contributions: the framework investors use

There is no formula for valuing a pre-formation IP contribution, but there is a framework that produces defensible results and gives co-founders a common language for the negotiation.

Stage of development matters most. An idea, even a brilliant one, has less value than a working prototype, which has less value than a validated technical approach, which has less value than a product with early customers. The further along the IP is when it is contributed, the stronger the argument that it represents significant value that should be reflected in the equity split.

Market comparables are relevant. If similar technology has been licensed, acquired, or spun out of research institutions at valuations that can be referenced, those comparables help establish a range of reasonable value. Biotech and deep tech startups frequently have access to comparable licensing deals that anchor the conversation.

What would it cost to recreate it? One practical valuation approach is asking what it would cost the company to develop the equivalent technology from scratch, using market-rate talent and time. If the contributed IP represents two years of a senior engineer's work, and that engineer's market salary is $250,000 per year, the replacement cost is approximately $500,000. That figure is not the value of the IP, but it provides a floor for thinking about the contribution.

What is the IP worth without the company? Pre-formation IP that has no commercial application outside the startup context is worth less than IP that could be licensed to multiple parties. Technology that only works in the specific context the startup is building for should be weighted accordingly.

What does execution contribute? The most important corrective to overvaluing pre-formation IP is recognizing how much of the company's ultimate value will come from execution: building the team, raising capital, finding customers, iterating the product, and scaling the business. For most startups, including most deep tech startups, execution is where the majority of the value is created. A structure that gives a technical founder 80 percent equity for their IP contribution and leaves 20 percent for everyone else will struggle to attract talent, investors, and additional co-founders.

Common structural approaches

Once co-founders have developed a shared understanding of the relative value of the IP contribution, there are several ways to reflect it in the equity structure.

Adjusted equity split at founding

The most straightforward approach is simply adjusting the initial equity split to reflect the IP contribution. If two co-founders would otherwise split equity 50-50 based on their forward-looking contributions, but one is also contributing significant pre-formed IP, the split might be adjusted to 60-40 or 65-35 in the IP contributor's favor.

This approach is simple, clean, and easy to explain to investors. Its limitation is that it forces co-founders to agree on the value of the IP contribution before there is any market evidence of what that value actually is, which can produce either over- or undervaluation.

IP licensing rather than assignment

Rather than assigning the pre-formation IP to the company in exchange for equity, the contributing founder licenses the IP to the company and retains ownership. The license can be exclusive, royalty-bearing, and perpetual, with terms that reflect the IP's value.

This approach has some appeal for founders who are uncertain whether the startup will succeed and want to retain the ability to use their IP in other contexts if the company fails. But it creates serious problems for investors. Institutional investors almost universally require that the company own its core IP outright rather than license it from a founder. A licensing structure where the company's most important technology can be revoked, modified, or subjected to founder disputes is not a fundable structure for most institutional capital.

If a licensing approach is considered, it should be understood from the outset as a temporary structure that will be converted to a full assignment before any institutional fundraise.

Milestone-based equity adjustment

Some founding teams use a structure where the initial equity split reflects forward-looking contributions, and additional equity is granted to the IP-contributing founder upon achievement of milestones that validate the technology's value. If the technology works as expected and the company hits defined technical milestones, the contributing founder receives additional equity. If the technology underperforms, the additional grant does not vest.

This approach aligns incentives well and avoids the need to value the IP precisely at founding. Its complexity is the main disadvantage: the milestone definitions need to be specific and objective, and disputes about whether milestones have been achieved are a common source of co-founder conflict.

Separate compensation for IP transfer

In some structures, particularly where the IP contribution has a clear and verifiable value, the company pays the contributing founder for the IP separately from the equity split. This payment might be in cash, in a promissory note, or in a combination of cash and equity separate from the founding equity pool.

This approach works best when the IP can be genuinely valued — for example, when it has been previously licensed at a documented rate or when comparable transactions exist. It separates the IP compensation from the equity split, which keeps the equity conversation cleaner and makes it easier for all founders to feel that their ongoing contributions are reflected in their equity position.

The documents that make it work

However the equity structure is designed, the following documents need to be in place before any work begins under the new structure.

IP assignment agreement

The contributing founder must sign a written IP assignment agreement that transfers ownership of the pre-formation IP to the company. As discussed throughout the previous posts in this series, without a written assignment, the IP belongs to the individual founder regardless of what anyone understood or agreed to informally.

The assignment agreement should specifically identify the IP being transferred, cover all rights in that IP including patents, copyrights, trade secrets, and know-how, include cooperation obligations for future patent prosecution and enforcement, and recite adequate consideration (typically the equity issued in exchange for the assignment).

If the IP includes patent applications or issued patents, the assignment needs to be recorded with the USPTO to put third parties on notice of the transfer. An unrecorded patent assignment is valid between the parties but does not protect against a subsequent purchaser who takes without notice.

Founder equity agreements with vesting

Every founder, including the IP-contributing founder, should have a restricted stock agreement with a vesting schedule. The IP contribution justifies a different initial equity percentage; it does not justify a departure from vesting. Investors will expect all founders to be subject to vesting, and a founding structure where the IP contributor holds fully vested equity from day one is a red flag in due diligence.

The vesting schedule for the IP-contributing founder may include a larger cliff or faster initial vesting to reflect the value already contributed, but some form of forward-looking vesting should be present.

Co-founder agreement

A co-founder agreement that addresses the equity structure, the IP contribution, each founder's role and responsibilities, decision-making authority, what happens if a founder leaves, and how disputes will be resolved is worth drafting even if it feels premature. Most co-founder disputes are about things that could have been addressed in a co-founder agreement if anyone had thought to write one.

The co-founder agreement should reference the IP assignment and the equity structure, confirm each founder's understanding of the basis for the split, and establish the process for resolving future disagreements.

How investors look at IP contribution equity structures

Investors evaluate IP contribution equity structures through two lenses: whether the IP is cleanly owned by the company, and whether the equity structure reflects a reasonable assessment of each founder's contribution.

Clean IP ownership is the threshold requirement. If the IP assignment is not in place, the discussion about equity structure is secondary to fixing the ownership problem.

On the equity structure itself, investors are looking for structures that make sense and that they can explain to their LPs. An equity split where one founder owns 85 percent of the company because they contributed IP is harder to fund than one where the split is 60-40, all founders are subject to vesting, and the rationale for the differential is clearly documented. Extreme splits raise questions about whether the non-majority founders have enough incentive to stay and build the company.

Investors also look at whether the IP-contributing founder's equity is subject to vesting. A large equity grant with no vesting represents a governance risk that most institutional investors will require to be addressed before closing.

Frequently asked questions

Should the IP-contributing founder always get more equity?

Not always. The equity split should reflect the totality of each founder's contribution, including the IP. If the IP is early-stage and unproven, its contribution to the equity split may be modest. If the company's entire business model depends on mature, defensible IP that took years to develop, the contribution is substantial. The IP contribution is one input into the equity conversation, not the only one.

What if the IP was developed with university or employer funding?

This is a critical question that needs to be resolved before the IP can be contributed to a startup. Universities and employers who funded the development of IP often retain rights to it through research agreements, employment agreements, or institutional IP policies. Contributing IP to a startup that is subject to a third-party claim creates a serious problem that will surface in due diligence. If there is any possibility that a university, employer, or research institution has rights in the IP, get a legal opinion before the founding documents are signed.

Can we structure the equity split differently for tax purposes?

The equity structure should be designed to reflect the actual founding contributions, not to optimize for tax outcomes at the expense of economic reality. Tax considerations are relevant but should not drive the fundamental structure. Work with both legal and tax counsel when structuring the founding equity to ensure the structure is both legally sound and tax-efficient.

What happens to the equity structure if the contributed IP turns out to be less valuable than expected?

If the IP was overvalued in the founding equity split and the technology underperforms, the equity split cannot typically be retroactively adjusted. This is one reason milestone-based equity structures can be appealing — they tie the IP contributor's additional equity to demonstrated value rather than projected value. For straightforward adjusted equity splits, the risk of overvaluation falls on the other founders, which is one of the arguments for being conservative in valuing pre-formation IP contributions.

Do we need a lawyer to structure co-founder equity with an IP contribution?

Yes. The combination of IP assignment, equity structure, vesting, tax elections, and co-founder agreement involves enough legal complexity that attempting to structure it without counsel creates meaningful risk. The cost of getting it right at founding is a small fraction of the cost of fixing it later, and most of the problems that kill deals in due diligence are things that experienced startup counsel would have caught and addressed at the start.

Structuring equity when co-founders contribute IP is one of the most consequential conversations a founding team will have. The structure you put in place in the first 30 days will define the economics of every financing, every acquisition conversation, and every founder relationship for the life of the company.

Getting it right requires honest assessment of what each founder is contributing, clear documentation of the IP transfer, vesting structures that align everyone's incentives, and agreements that put the understanding in writing before there is any value at stake to dispute.

If you are structuring a founding team with IP contributions and want help getting the documents right from the start, contact Ana Law to schedule a strategy session.