Article

Apr 8, 2026

What Investors Look for in IP Due Diligence Before a Series A

Investors scrutinize your IP before writing a Series A check. Learn what they look for, what kills deals, and how to get your IP house in order before you raise.

IP due diligence is where a lot of Series A deals slow down, get repriced, or fall apart entirely. Founders who have been heads-down building their product often arrive at the due diligence phase assuming their IP is fine because they have not had any legal problems. That assumption is wrong often enough that it has become one of the more reliable ways to identify founders who have not worked with experienced startup counsel.

Investors conducting Series A due diligence are not looking for perfection. They are looking for risk. Specifically, they want to know whether the company actually owns what it says it owns, whether anyone else has a legitimate claim to the technology, and whether the IP portfolio is defensible enough to protect the business they are about to fund. Problems that surface during due diligence become leverage: they delay closings, they produce price chips, and serious problems kill deals that otherwise would have closed.

The good news is that most IP due diligence problems are avoidable. They arise from things founders did not do early on — or did not do correctly — and they can be fixed if you catch them before the term sheet arrives. This post covers what investors actually look at, what they find most often, and what to do before you start your raise.

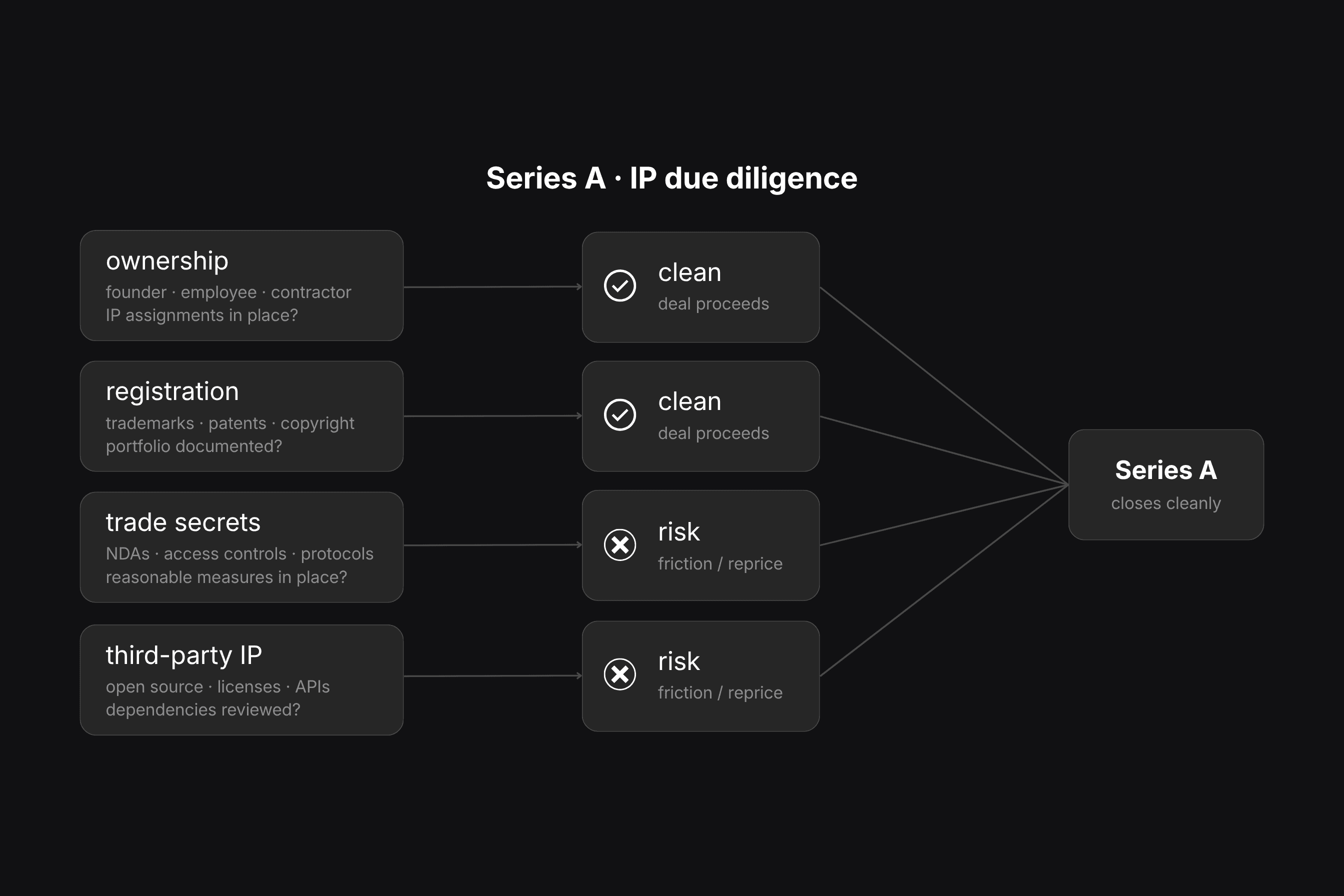

Ownership: does the company actually own its IP?

This is the threshold question in every IP due diligence review, and it is where the most deals break down. Investors are funding a company based on the value of its technology. If that technology is not clearly owned by the company, the investment thesis falls apart.

Founder IP assignments

When a startup is formed, any IP that founders created before formation — including code, designs, prototypes, business methods, and written materials — needs to be formally assigned to the company. This seems obvious but is frequently not done, or is done informally without a written assignment agreement.

If a founder built the core technology before the company was incorporated and never signed a formal IP assignment, that technology may legally belong to the founder as an individual rather than the company. From an investor's perspective, this means they are funding a company that does not own the technology it is selling. The fix is straightforward — a written assignment agreement — but if the founder relationship has deteriorated by the time due diligence surfaces the problem, getting the assignment signed can become complicated and expensive.

Investors will ask for copies of IP assignment agreements from every founder. If those agreements do not exist or are incomplete, expect the deal to pause until the issue is resolved.

Employee and contractor IP agreements

Every employee and contractor who has contributed to the company's technology needs to have signed an agreement that assigns their IP to the company. This includes engineers who wrote code, designers who created brand assets, researchers who developed methods, and anyone else whose work is embedded in the product.

Standard employment agreements include IP assignment provisions for work done within the scope of employment. Contractor agreements need explicit assignment clauses because the default rule for independent contractors — unlike employees — is that the contractor, not the company, owns the work they create. A contractor who wrote significant portions of your product and never signed an IP assignment may have a legitimate ownership claim to that code.

Several states, including California, Delaware, and Washington, have statutes that limit the scope of employee IP assignments. California Labor Code section 2870, for example, protects employees' rights to inventions developed entirely on their own time without company resources and unrelated to the company's business. Investors will look for whether your IP assignment agreements comply with applicable state law and whether any employees have asserted rights under these carve-outs.

Prior employer claims

If your founders or key engineers came from other technology companies, investors will assess whether those prior employers might have a claim to the technology your company is building. Most technology employment agreements include invention assignment provisions that are broader than the California carve-out allows, and some are aggressively worded.

The specific concern is whether any of your company's core technology was developed using prior employer resources, during prior employer work time, or relates to work the employee was doing at the prior employer. If the answer is yes to any of these, the prior employer may have a claim. This is not hypothetical — there are documented cases of startups having to defend against prior employer IP claims during or after fundraising.

Investors will ask founders and key technical employees to describe their prior employment and whether any of the company's technology was developed in circumstances that could create prior employer claims. Honest answers are essential. Misrepresentations discovered after closing create indemnification obligations and reputational damage that far exceed whatever discomfort the honest answer would have caused.

Registration: is the IP portfolio documented and protected?

Ownership is the threshold question. Registration is the next layer. Investors want to see that the company has taken affirmative steps to protect its IP, not just that it exists.

Trademark registrations

Investors will check whether the company's brand — its name, logo, and any distinctive product names or slogans — is protected by registered trademarks. An unregistered brand is vulnerable. A competitor can register a similar mark in key markets, a trademark troll can file first in a jurisdiction you have not covered, and without registration you have no ability to use customs enforcement to stop infringing imports.

They will also look at the clearance search history. If the company adopted its brand name without conducting a professional trademark clearance search, there may be conflicting registrations that create infringement exposure. Undisclosed infringement risk is a significant due diligence finding.

Patent coverage

Not every startup needs patents, and investors understand this. But investors will assess whether the company has identified patentable innovations, made deliberate decisions about whether and what to file, and documented its reasoning. A company that has never thought about its patent strategy is a different risk profile from one that has evaluated its technology and made an informed decision to rely on trade secrets or first-mover advantage instead.

For companies that have filed patents, investors will review the prosecution history, assess the breadth and quality of the claims, and look at whether the portfolio covers the technology that is actually central to the business. A patent on a feature that is not core to the product provides less protection than investors want to see. Broad claims covering the company's core differentiation are what move the needle.

Investors will also look at whether the company has conducted freedom-to-operate analysis on its core product. If the product potentially infringes an existing patent and the company has never assessed that risk, it is a material undisclosed liability.

Copyright in code and content

Investors will assess whether the company's codebase has been reviewed for open-source license compliance. Code that incorporates open-source components under copyleft licenses like GPL may impose obligations on the entire codebase that affect how the product can be commercialized or licensed. A company that has been using GPL-licensed code in a proprietary product without understanding the license implications may have a significant legal problem it does not know about.

Trade secrets: are confidential assets actually being protected?

Investors will assess whether the company is treating its confidential technical information as trade secrets — which requires active protective measures, not just an intention to keep things private.

The specific things they look for: confidentiality agreements with all employees and contractors, NDAs with vendors and partners who receive access to technical information, access controls limiting who can see sensitive technical information, and departure protocols that include reminders of confidentiality obligations and return of company materials.

A company that has been sharing its model architecture, training data, or core algorithms with vendors, partners, or even potential customers without NDAs has been diluting its trade secret protection every time it did so. This is one of the most common findings in due diligence for AI and deep tech companies, and it is entirely avoidable.

Third-party IP: what did you build on?

Investors will look at whether the company's product incorporates third-party IP and whether the rights to use that IP are properly documented.

This includes open-source software licenses, as discussed above, but also licensed datasets, stock imagery, third-party APIs, and any other content or technology that the company did not create itself. Every material third-party dependency should have a license that clearly permits the company's intended use, and those licenses should be reviewed for restrictions that could affect the company's ability to commercialize, distribute, or sublicense the product.

For AI companies, training data provenance is a specific and increasingly scrutinized due diligence area. Investors funding AI startups are now routinely asking how the training data was obtained, whether it was properly licensed, and what the company's exposure is to the training data copyright litigation that is currently working through the courts.

What kills deals and what just creates friction

Not every IP due diligence finding kills a deal. Experienced investors distinguish between problems that go to the fundamental value of the company — ownership gaps, material infringement exposure, prior employer claims to core technology — and problems that are real but fixable, such as incomplete assignment agreements with minor contributors, minor open-source compliance issues, or trademark gaps in non-priority markets.

Deal-killing findings typically share one characteristic: they call into question whether the company actually owns what it is selling. If the technology that underlies the product is not clearly owned by the company, no amount of revenue or traction will save the deal. Investors are not in the business of funding ownership disputes.

Friction-creating findings are the ones where the problem is real but the fix is straightforward. Missing contractor assignments, incomplete trademark coverage, undocumented trade secret measures — these create deal friction, produce price chips, and generate representations and warranties in the investment documents that shift risk to the founders if the problem resurfaces. They rarely kill deals if they are disclosed promptly and addressed cooperatively.

The difference between a finding that kills a deal and one that creates friction is often how the founder responds when it surfaces. Founders who acknowledge the issue, have a credible plan to fix it, and demonstrate that they understand why it matters tend to fare better than those who minimize or become defensive.

How to prepare before you start your raise

The time to address IP due diligence issues is six to twelve months before you expect to receive a term sheet, not after.

Commission an IP audit. Have counsel review your IP ownership chain, your registration portfolio, your open-source compliance, and your trade secret protection measures. Identify the gaps before investors do.

Collect and organize your IP documentation. Gather every IP assignment agreement, employment agreement, contractor agreement, NDA, trademark registration certificate, patent filing receipt, and license agreement into a clean data room. Due diligence moves faster and creates less anxiety when the documents are organized and accessible.

Fix the fixable problems. If there are missing assignments, get them signed. If there are trademark gaps in priority markets, file applications. If there are open-source compliance issues, address them. If NDAs are missing from key vendor relationships, execute them now. Most IP due diligence problems can be resolved before the raise begins if you find them early enough.

Document your IP strategy. Be prepared to articulate your IP strategy clearly: what you have filed, what you have decided to protect as trade secrets, what freedom-to-operate analysis you have done, and how your IP portfolio relates to your competitive moat. Investors are evaluating whether your team thinks carefully about IP, not just whether your paperwork is complete.

Frequently asked questions

When should a startup start thinking about IP due diligence preparation?

Ideally from day one, but practically speaking, the latest you should start is 12 months before you expect to raise a Series A. Many of the most common IP problems — missing founder assignments, contractor IP gaps, trademark conflicts — are much easier and cheaper to fix when the company is small and relationships are intact than when you are under deal timeline pressure.

What is the most common IP due diligence problem investors find?

Missing or incomplete IP assignments from founders and early contractors. It is the most frequent finding and the one with the most direct impact on deal structure. The fix is straightforward when caught early and complicated when the relationship with the relevant person has changed.

Do investors always hire outside counsel to conduct IP due diligence?

At the Series A stage, institutional investors almost always engage IP counsel to conduct at least a preliminary review of the company's IP portfolio and ownership chain. The depth of the review depends on the investor, the industry, and the importance of IP to the investment thesis. Deep tech, AI, biotech, and other IP-intensive companies receive more thorough reviews than software-as-a-service businesses where the IP portfolio is less central.

What representations and warranties about IP will I need to make at closing?

Standard Series A documents include representations that the company owns all IP material to its business free and clear of liens and encumbrances, that the company has not infringed third-party IP, that no third party has asserted a claim against the company's IP, and that the company has taken reasonable steps to protect its trade secrets. Breaches of these representations can create indemnification obligations, so understanding exactly what you are representing is essential before you sign.

Can IP problems discovered during due diligence be negotiated around?

Sometimes. Minor problems can be addressed through representations, warranties, and indemnification provisions that shift the risk of the problem materializing to the founders rather than the investors. Major problems, particularly ownership gaps in core technology, are harder to negotiate around because the investor's thesis depends on the company owning what it says it owns. The best negotiating position is one where the problems have already been fixed before due diligence begins.

IP due diligence is not something that happens to you at the Series A. It is something you prepare for from the day you start building. The founders who sail through due diligence are the ones who treated IP ownership, registration, and protection as operational priorities from the beginning, not the ones who scrambled to fix problems after a term sheet arrived.

If you want to prepare your IP portfolio for a fundraise or work through a pre-raise IP audit, contact Ana Law to schedule a strategy session.